Time to Panic?

Or, What is Going On!?

As one might imagine, I’ve been getting a lot of questions over the past 24 hours. More than usual. We have several critical events moving in parallel, so this is going to be a long one. I’ve broken it up into sections and subsections for those who want to read each part, or for the real wild people among us, just start rolling and do the whole thing.

I normally say this only at the end, but my contact info is at the bottom. If you need my services, or you are a regulator/legislator and just need help (free, for you guys), reach out.

So what am I going to address today?

What happened with SVB?

What is the localized impact of SVB failing?

Are there going to be runs on other banks, and are we about to have another 2008 or S&L crisis?

Circle and the topic of “stablecoins”

Let’s do this.

What Happened With SVB?

The Rise

As you may have heard, we just had the 2nd largest bank failure in the history of the United States on Friday (March 10, 2023, RIP Silicon Valley Bank). Suffice to say this is not news that can really have much of a positive spin put on it.

The SVB story is, unfortunately, very similar to the issues at Silvergate. To avoid re-hashing a lot of the same material in anything other than summary form, if you haven’t read my post on Silvergate, go read that.

To give the brief background, Silicon Valley Bank was founded in 1983, and fundamentally specializes in providing banking services to technology and life sciences companies. It is based in, unsurprisingly, Santa Clara, and has long been a bastion of the tech community and has linkages to many of the major tech, venture capital, and adjacent firms in the ecosystem.

SVB had a reputation for being front-footed on technological risk, solid understanding of the tech ecosystem, their own ventures arm, and was, in general, not considered to be particularly remarkable from the core banking side of things.

So how did a bank like this blow itself up in spectacular fashion, such that the demise of SVB was basically the fastest bank run in American history and it went from semi-operational to literally dead in under 48 hours?

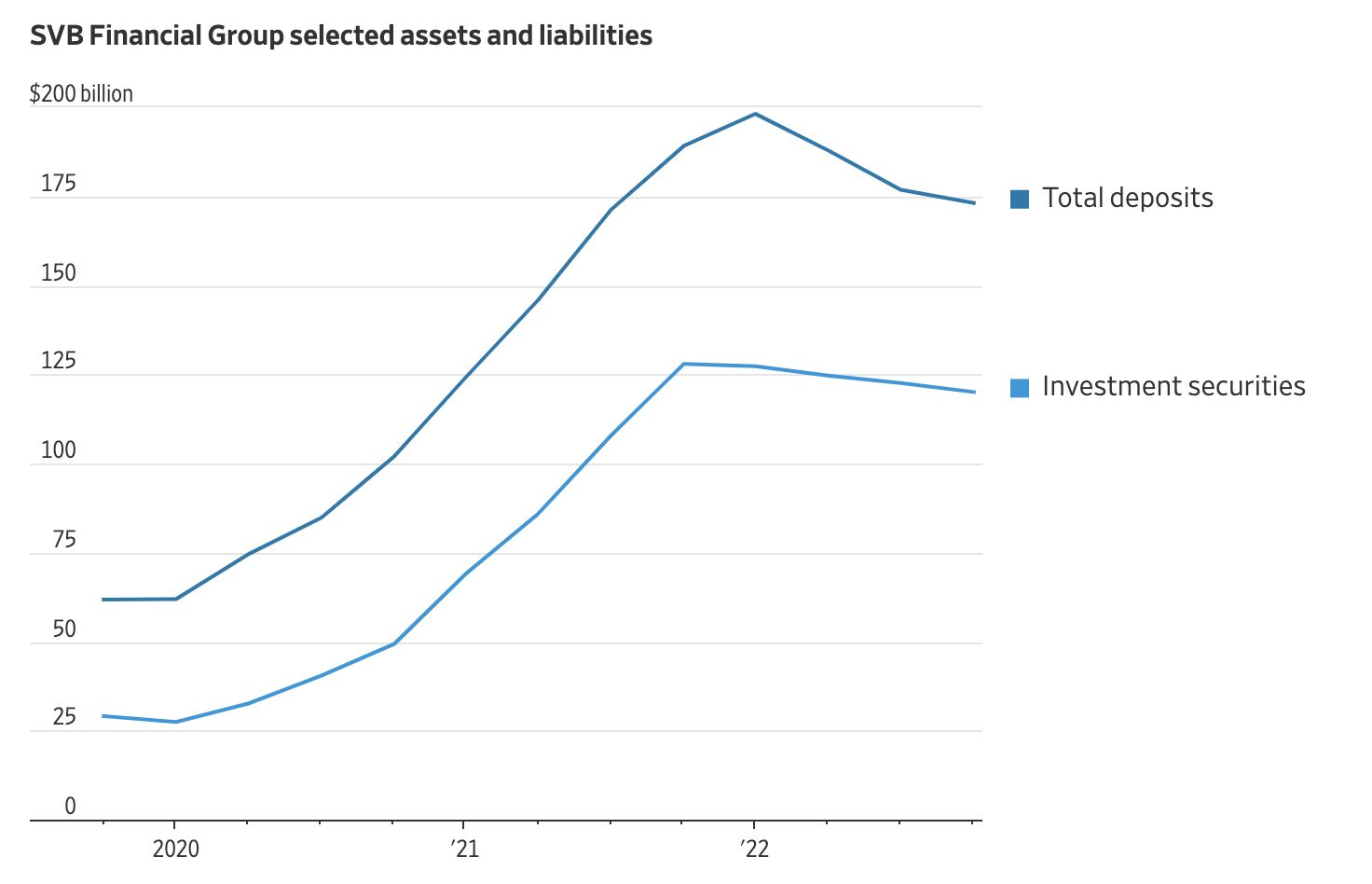

First, we have to start with COVID. During the pandemic, there was a very dramatic expansion of money supply in order to offset the effects of everything shutting down. A large beneficiary of this situation was the tech sector, as everyone was stuck at home and all-virtual forever all-everything became the investment thesis at the time. VC funds, tech unicorns, and the valley in general had a massive boom in terms of cash and funding. As a result, this happened to SVB’s balance sheet:

That’s a big increase! And as you can see, most of that increase did not go into loans, but rather, into investment securities. Notably, the fact that their balance sheet almost tripled in size directly concurrent with the pandemic meant that when the tide went back out on the stimulus, it was entirely possible that the deposits would go out with them.

As a treasury and risk person at a bank, when you have that kind of deposit inflow, you have to make a judgment call. Your options are essentially the following:

Refuse the deposits, either explicitly or by making the economic terms so poor people move them elsewhere.

Take the deposits, but expect them to be hot money and leave quickly, and thus invest them very conservatively in things like t-bills, ON reverse repo, or other such highly liquid and easy to unwind instruments.

Take the deposits, and assume that we are in a new paradigm where this time is different and thus go invest them in long-dated things to earn “more”1 to juice your profits.

Obviously, #1 is not going to make your management or your customers happy. This is genuinely hard to do. I’ve seen very few banks that have the stomach to just tell potential customers to go away. It does happen once in a while, but it takes above average management with significant confidence to run this playbook.

#2 is probably the smartest move overall, if you can make the economics work. This gives you maximum optionality. It is more work to onboard a bunch of people who might just rampage right back out the door, but the reality is that other than the work and the effort to make sure the risk is managed, there’s little downside here. If both SVB & SI had done this, they’d both still be standing. Even so, there’s inexplicably a severe allergic reaction to the idea of “how about we not lend all this money out in risky ways” at a bank. I can’t explain why. Sometimes it even rests on management misunderstanding of economics2, as shockingly few people truly understand how fixed income works.

#3 is, unfortunately, what most people do. I find it personally confounding every single time this happens, but it’s also the most common thing to happen, so maybe I am the problem here for thinking people should do something else? Either way, this path obviously ends in disaster if things don’t break exactly the way you planned for. If rates go up instead of down, and deposits leave, you are now a forced seller at a loss. Do you know what that means for a bank?

The Fall

At the same time SVB was experiencing those massive gains in deposits, they decided to run play number 3 from the list above. To the best of my knowledge, SVB had an average duration of roughly 4 years for their securities portfolio, and those securities consisted of things like Agency MBS, not just US Treasuries.

For those uninitiated in the complete and total nonsense that is fixed income pricing, here are some basic rules of thumb so you know what happened to the balance sheet at SVB:

Rates and bond prices move in opposite directions. If rates go up, bond prices go down. If rates go down, bond prices go up.

Bond prices change in response to rates by a percentage equal to duration * change in rates, as a rule of thumb3

So with those rules in mind, here is what SVB did: they bought bonds back when interest rates were about 4% lower than they are now, and they bought bonds with about a 4 year-ish duration. What this means is that as the Fed raised rates, SVB lost money on those bonds. In this example, they lost about 16% on those bonds (approximate at best), so if they had bought, oh, $100B of bonds for the deposit growth, they are now down $16B on that.

Which is more than the equity of SVB was worth.

Now I am going to tell you something that is probably going to surprise many of my readers: this happens all the time in banking. Why are banks not constantly dying because of it, then?

First, banks have two forms of accounting they can elect for assets. One is called Held-to-Maturity (HTM), which means you don’t account for gains or losses and just hold the thing as though you will, with certainty, hold it until it matures. This one doesn’t require any change in value unless there is an impairment. The other option is Mark-to-Market (MTM) accounting, which means that you have to price your securities and loans at the price you could sell them for in the open market as of that day.

Which one of these is correct?

That actually depends on the funding base of the bank. If you have long-term funding and can match your obligations with the tenor of your assets, HTM accounting is actually pretty appropriate. If I have a 4yr bond and a 4yr loan against that bond, that’s great! If you have short-term funding that can depart at any time, then MTM is much more appropriate, as you can’t count on holding to maturity.

So how did things go wrong at SVB? They assumed their long-term bonds were matched by long-term deposits, but as it turns out, those were short-term deposits. This is the essence of many bank runs, and is exactly what happened here.

As depositors left, they were forced to sell what had been HTM positions, which crystallized losses, which makes more people worried, which causes more withdrawals, which causes more deposits to leave… you see where this is going:

What is the Impact of SVB Failing?

Here is where things get interesting. I’m going to start by explaining the common narrative that I am seeing on Twitter and in the popular discourse, and then I’m going to explain what is actually going on.

Popular Narrative

“Wait a minute, SVB is just a bank for rich venture capital folks. If you had over $250k of money there, you can take a loss. Why should we bail out rich bankers!?”

This is basically almost every variety of take that I have seen about SVB, and it relies upon two fundamental misunderstandings of the structure of a bank.

The first is that somehow depositors are always rich and/or investors in the bank. The second is that plugging the deposit hole is somehow bailing out the bankers.

In this scenario, where we would end up is a slow or semi-functional resolution for the bank, in which large amounts of deposits are locked up for an indefinite period of time, and when they are released, might be worth 50-80 cents on the dollar.

We can call this scenario 1.

What’s Actually Happening

Now, let’s talk about how FDIC coverage at a bank works, and how the capital stack of a bank works.

First, FDIC coverage applies to single persons4 up to $250k of deposits. This means that if you had money at SVB, and it fails, and that money is less than $250k, you are almost certainly fine. That money will leave first, and everyone else gets to fight over the scraps. Now, if the FDIC itself fails, that coverage isn't worth much, but that's a true end-game scenario as that didn't even happen in 2008. Also important to know is that that is $250k per bank, meaning if you have multiple accounts at one bank that add up to more than $250k, you have a problem! However, if you have over $250k, but it's at like six different banks and they are all below $250k, that's good.

Why does it work this way? I don’t make the rules.

Second, we need to talk about the kinds of accounts that you find at these banks. The natural tendency of humans is to generalize from their individual situation, so a common refrain is “well, anyone with over $250k should have spread out their money!”. To that I say this:

Well, duh.

If you were a person in the sense we mean, like a two-legged human being.

But what if you were not? What if you were a legal person? What if that legal person is a corporation that needs to make payroll? A local grocery store chain taking payments and then paying for inventory? The donation account for a charity?

There are many kinds of “persons” at a bank, and most of the ones that are over FDIC limits are typically not what we mean when we say “Joe is a person” but rather what lawyers mean when they say “Santa Clara Firefighters Pension Fund is a person”.

Capital Stack

Let’s also take a moment to talk about the typical capital stack of a bank. By this, I mean money that has been “invested” in a bank in various ways, and as you can see, I am going to use invested pretty loosely here. These are the major components:

Equity, which is actual money invested by (hopefully) sophisticated investors. Here, they know their money is at risk, as they take the first losses when things go wrong. As a result, they also get an outsized share of the gains. For a company like SVB which is public, this is a combination of active fund managers, passive index funds, hedge funds, and private investors who all can purchase shares. In general, these people are supposed to be informed, do their own research, and understand the risks that they are taking when they invest in this thing. I would suggest that when a bank fails, unless it failed because management perpetrated a massive fraud on these people, you shouldn’t have much sympathy for them. Why? Failure was literally the risk they were being paid to take.

Bondholders, which are people who lent money to SVB and were senior5 to the equity holders. These people typically lend an amount of money, to be repaid at a specific later date, and are paid interest along the way. That kind of thing is called a bond. There's a lot of them out there in the world, and you've probably heard of Treasury Bills, Bonds, or Notes before6. These people also tend to be sophisticated investors, just like the equity holders.

Deposits, which are the deposits of people at the bank. Most people don’t realize this, but technically when you deposit at a bank, you are lending that bank money! Yes! I mean it! I know that sounds crazy, but it is true. However, this is not where the sophisticated investors are. Most people don’t go to the bank and go “ah, yes, [Insert local community bank here], I will lend you money expressly for you to make loans because I want to make a profit”. They give money to banks because they want someone to hold it for them and connect it to a banking system so they can later pay for things, not lose it, and generally treat it like money locked in a box. Thus, these people are fundamentally different in their sophistication about evaluating bank balance sheets (none) and their purpose for being there (they are using the product, not making a profit).

Why did I explain all this? It will become important when we discuss fallout, which we will do now.

Fallout Directly Related to SVB

We defined scenario 1 above, so let’s talk about that now: in scenario 1, when the bank fails, persons7 get $250k back, and should get that back on Monday. However, the rest becomes some kind of estimated return from the FDIC and then an unsecured creditor thing that can best be described as an IOU of somewhere between real and highly dubious value. In the case of IndyMac, this was 50% or so.

So to talk about our capital stack above, equity is gone, bonds are gone, but deposits? Also kind of gone.

In this case, you’re going to have complete fucking chaos. Multiple firms likely cannot make payroll, pay vendors, or function appropriately come next week as their cash on hand is wiped out. This is less of a problem, in some ways, for companies that were hoarding cash and it was their runway (so VC-style companies) but way more of a problem for operating companies because if that was your operating capital, then…?

Yeah.

The other problem is that SVB served as a bank for several payments and payroll processors, so all of that stuff is likely fucked beyond all recognition if there are major haircuts for anyone who was using them at scale. Again, this is not what people typically think of for banks, but it is actually the stuff more likely to break and more contagious, because what you could have is massive layoffs, disruptions, failure to pay vendors, and more for a lot of businesses in the tech space and local California space.

Now let us consider the other option, which we are going to call Scenario 2, which is going to be derided in the popular press (or at least some economically illiterate quarters of it) as a bank bailout.

In this case, where the “rich bankers” are being “bailed out”, here is what the recoveries are going to look like: equity is wiped, bonds are wiped, but deposits are almost entirely (if not completely) safe.

I want you to pause, consider what we said about capital stack before, and ask who got bailed out here. The investors? Toast. The employees and executives paid in stock for their giant bonuses? Toast. The venture capital and private equity funds that invested in the bank? Toast.

You know who is not toast? The depositors who were using the bank as customers. Some of those people, yes, will be rich people and some will be angry that they were “bailed out” (even though in this case, it’s unlikely those people were investing for a profit because you wouldn’t be a depositor if that were the case!). Many more of those persons will be corporations making payroll, paying vendors, and the like. A lot of them might be things like startups, partnerships, or banking-as-a-service clients for a bank like SVB. These are not typically the things you expect to be completely wiped out, and making sure your building facilities people get paid or that the non-profit donation account doesn’t get wiped out are not the “rich” we rail against in a bailout.

As a general matter, in scenario 2, contagion is very limited. Yes, there are some equity losses and a handful of unlucky people who went super big on SVB are going to end up bankrupt. Bondholders might be ticked, if there are many of them. But all of these people knew the game and this is what they signed up for. C’est la vie.

On the other hand, there is minimal disruption to the depositors and regular main street types of business. The chaos from scenario 1 is limited. Here, it’s almost… boring that the bank failed. Your bank account probably gets re-labeled as a new bank takes over and continues onwards after the equity and bondholders get wiped. So congrats, you are now customers of Goldman Sachs US Bancorp or some such.

I think it is pretty obvious one of these outcomes is both better and fairer than the other, and yet it’s the one decried for being a bailout. I hold the view that this mostly comes from a lack of understanding about how a bank is structured and the role depositors play.

Are There Going to be Runs on Other Banks?

Now here is where things get interesting. First, I need to expose an important truth about bank runs that people gloss over completely: all banks have exposure to runs.

That is to say there does not exist a type of bank that can withstand a run. The question is how much damage it will do. The other question is the network effects of the run, as a run on individual banks works very differently than a run on the entire banking system, as this is a network problem.

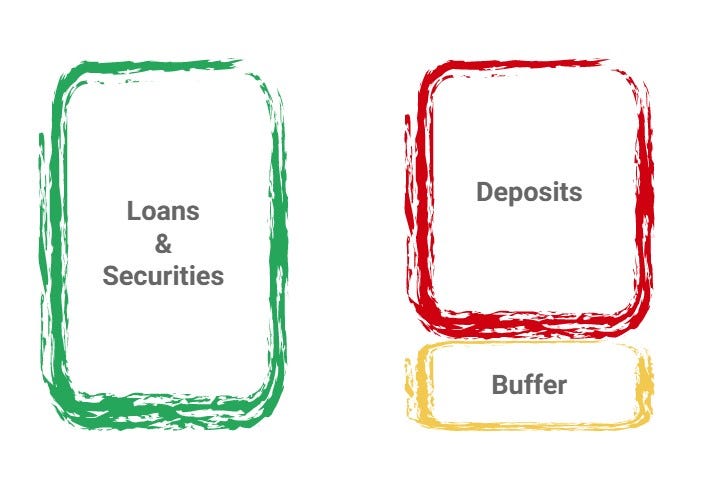

Let us start with the simple model that I had created in a previous post:

If that is our bank balance sheet, then one of the things you can see is that banks have some buffer of equity in normal cases, and then beyond that, they have deposits. If 100% of the deposits leave, you… don’t have a bank? This is the definition of a bank run. In a literal, functional, basic sense, if you have mass deposit flight, you stop being a bank, because you stop having depositors.

The questions that ultimately matter to the depositors are the following:

Is everyone else going to take their money out?

If everyone takes their money out, can the bank unwind this whole thing and I get my money back, or do the depositors8 get screwed?

First of all, if there is strong confident in number 2, number 1 becomes less relevant. The problem is that most people have no idea how to assess this risk. Hell, I worked at a bank, traded the Bank-Owned Life Insurance (BOLI) wrap book9, which is a key part of tier 1 capital for US banks, and I can barely assess bank solvency from the outside sometimes. Expecting normal people to do this is ridiculous, and the logical conclusion most would draw is simply either not to use banks or only use banks so big that if they fail, we know they will be bailed out (e.g. the big 4).

Thus, bank CEOs are often left playing a very dangerous confidence game. Many fail at it (see: SVB), but the best of them not just succeed but inspire confidence. The problem is to do this you need charisma, knowledge, to have actually managed risk well, and to be willing to take all sorts of slings, arrows, and daggers in public. Perhaps the best at this in recent history is Jamie Dimon, who led JPM through 2008. I can still hear him saying “fortress balance sheet” in my head, because he said it so many times he must whisper that in his sleep now.

But it worked.

Here is why that matters so much: if the answer to number 2 is that people think they will get screwed, they know that they would take their money out if they can, so the answer to number one also becomes “well, obviously”. It is the Prisoner’s Dilemma. It would be better for everyone if we don’t collectively run the bank, but if people start running the bank, you want to have gone first. Therefore, people go first.

Once that process starts, it’s over. And what determines if that starts? The public perception that the bank won’t have enough money to pay out all the deposits, either because of losses on loans due to default, or losses on loans if they are a forced seller due to interest rates going up.

That last point is very relevant right now.

Other Bank Contagion

This is the problem regulators are grappling with. The profile of a troubled bank in this environment looks like the following:

Underwater on a securities or loan book with long duration loans made at low rates

Concentrated depositor base that could rapidly engage in flight

Low NIM compared to competitors (which is a tell they don’t have room to move up to retain depositors)

So if you are looking for banks that would be in trouble right now, I would suggest that is the profile most similar to SVB and Silvergate. I am less concerned about the giant banks with huge deposit bases, smaller banks with low duration risk and diversified deposit bases, or specialist banks where this really isn’t how they operate (see: State Street).

If you are a banking regulator at this moment, the question you are asking yourself about SVB is that if it goes down, will people start withdrawing deposits from other banks? Here is where we get to the uncomfortable truth about uninsured deposits: mostly people don’t think deeply about counterparty credit risk to their bank, so if you make them think about it, they basically panic.

The ideal situation for a regulator is that people stay calm and don’t start stampeding away from other banks, as once that starts, the logical conclusion is a US banking system where you have 10-ish huge banks, a handful of key specialists, and everyone else is a corpse. That is not great for long-term competition or short-term stability, as one might imagine.

So how do you stop that from happening, and why would SVB not kick off a mass contagion event for the US banking system?

First, you want to resolve the SVB situation without depositors taking a haircut. Quite bluntly, recoveries for the bondholders and equity holders are simply not a priority in this situation, but depositors are. If the FDIC, who has been working quite hard over the weekend and has run this process many times since 2008, can broker a sale where the depositors are made whole, there will be much more confidence in the system overall going forward (unless this keeps happening over, and over, and over).

Second, if you can’t do that, you consider seriously backstopping the depositors. Again, not the bondholders or the equity, but if you allow SVB to open on Monday with a “yeah, um, so if you were a depositor, we just don’t know, maybe you get your money back but also maybe not and we don’t know when”, people are going to do the hyper-panicked speedrun just assume it’s all dead version of the thing I said above and runs are likely to start on many other banks. This is a bad situation. That’s why there are rumors out there of the Fed creating a facility to stop this if it starts in other places.

Third, you have to project confidence and get in front of rumors of other runs. To some extend, this is the hardest problem as you are now reliant on people from multiple agencies coordinating information and the bank executives themselves not saying dumb things. Bad outcomes here increase the reliance of solutions in the first and second point, as one can imagine.

Lastly, there is something of a network effect issue here. When people “take their money out of a bank”, that can mean one of three things:

They send it to another bank

They put it in securities or a money market fund

They literally ask for cash and put it in a hole in the ground or something

These all have very different implications for the system. Obviously, situation number one means your total deposits are unchanged, but the location has changed. This can lead to collapses of banks and either diversification or consolidation, depending on context. The second and third are different: now your banking system is straight up losing money and people are reducing their exposure. In those cases, things start to get systemic and failures are cascading as opposed to localized. That is the 2008 scenario that caused the government to get so scared about the system, and is the one that everyone would be wise to prevent this time around.

Predictions

So to put my money where my mouth is, what do I think will happen?

I don’t think the regulators in the United States want to risk a massive, uncontrolled tailspin. I also don’t think they want to be seen as offering an unlimited bailout to people who took significant risks and then got immolated because of it. Therefore, I am going to predict a middle road solution:

SVB is likely sold, probably but not certainly in parts, the depositors are going to make it out with a 100% (or very high 90s) recovery in short order, and the bondholders and equityholders are going to get completely wiped out. This would send the message that if you are a depositor, you don’t have to panic and we’ll take care of you, but if you are running a bank or investing in one, you’d better have your act together or if the reaper comes to your door, we’re not saving you.

Larger measures will come later, if there are bigger failures and more political will behind it. The reality is the optics of a significant “bailout” (even if people misunderstand that and it’s mainly the depositors) for a bank named Silicon Valley Bank (especially after the obnoxious bleating of the VC crowd on Twitter, which comes across as exceptionally tone-deaf) just aren’t something most politicians will go for… but neither is kicking off a chain reaction of bank failures that infects main street in shockingly short order.

So we are going to get a middle solution. Will it be enough? I actually think it might, with some important caveats that other similarly situated banks to SVB might also tank this week.

Non-Bank Collateral Damage

Now that we’ve talked about the banking angle, let’s talk about what might turn out to be the more important angle: the non-bank impact. SVB was a notable bank for VCs, supporting the startup ecosystem, and back-end functions for things like payroll processing. This is actually the mechanical stuff that matters a lot more, in some ways, and why all banks of sufficient size are at least somewhat “systemic” despite what anyone will want to say about them.

In plain English, if SVB fails in disorderly fashion, there’s a lot of firms that can’t make payroll, pay vendors, pay for inventory, etc. in the coming days, even if they eventually get a lot of that money back, and it will have knock-on effects to the real economy. In this specific case, probably primarily the California Bay Area economy, so that’s not particularly politically favorable for SVB, but that doesn’t change that people would lose jobs over this.

Even if SVB is rescued, however, I expect there will be impacts. One is going to be structural changes to how deals work. Banking diversification will be a thing, and reliance on one bank for serving a whole segment is pretty transparently dumb going forward. What that means is that competition for tech banking will increase, but as SVB was at the forefront, the shape and terms may be less favorable to the tech sector in the short and medium term. The shine is off the industry, and their biggest financial hub just imploded. It’s hard to take that as a short-term positive, even if a long-term shift in structure might be for the best.

Still, watch for the actual mainstream business impact. That is what could cause real bleeding if there is not satisfactory resolution.

Why Did USDC Break?

Speaking of stress in the market, check this out from Coinmarketcap:

I’m going to go out on a limb and say that’s not how a stablecoin is supposed to work! So what happened?

As it turns out, Circle was managing reserves for the stablecoin USDC by keeping a significant amount (allegedly about $11B) in bank deposits. Going back to what people mean when they say cash, they don’t literally mean cash in a vault, so Circle did this instead of getting much larger amounts of the reserve money into t-bills or other forms of securities.

It was revealed Friday that Circle might have exposure to SVB, and over the weekend, it became clear they held $3.3B of reserves at SVB, according to Circle themselves. That’s not great risk management about cash, but my thoughts on that are definitely too long for this blog post and I’ll be creating another one on how to manage funds for a stablecoin down the road. For now, let it just be said this meant that they had $3.3B minus $250k of FDIC coverage of exposure to SVB, potentially.

They also suspended withdrawals over the weekend (likely due to running out of cash at 24/7 fast payments rail banks, a traditional banking problem I have talked about before).

Now, is that real? There are two questions. The first is they attempted to wire money out, and allege they made the cutoff before the FDIC put the bank into receivership. If this is true (I have no personal knowledge), then they should get the money and there is not a hole. The second is even if they didn’t, are they going to recover on the deposits?

Some very rough napkin math is that if you had $3.3B of exposure against low $40B of outstanding, that’s ~8% of your total. So the point where USDC traded down below .92 either implies that people thought other banks were going to die and Circle would lose even more, that somehow the US treasury was going to default (the rest is in t-bills, remember), or that Circle had stolen the money and was off to the races. It’s indicative of a panic. There’s no fundamental reason for that. More so, if you understand recovery levels, then SVB is likely getting back at least 70% even in a very, very conservative scenario, so the actual trading level is more like 2-3% down, meaning USDC was likely a screaming buy beneath .97. Right?

Nerdy Stablecoin Mechanics

So one of the things to consider here is that we actually have to make some assumptions about how things are going, as there are well-founded reasons to believe that maybe USDC should be trading below .97. What are they?

One is how Circle redeems. If they actually had a 3% hole, and they allow 1:1 redemptions starting on Monday, what this actually means is that the first 97% of people to redeem would get $1, but the last 3% would get $0. That is definitely not .97! Neither of those numbers are! So if you believe Circle has a hole, but also is going to carry on like they don’t, and you don’t currently have a Circle account or way to redeem, you might just want to get off this train.

Two is that you might just have lost faith in Circle over this. One of the truisms of the stablecoin game is that people need to have confidence in the reserves and the mechanics of getting their hands on those reserves, but that’s fine. However, if you break that confidence either through poor management or through being in places where people doubt they can get the money out (either through lack of rule of law or through regulatory capriciousness) then you can have long-term doubts in your viability.

Three is people are actually thinking that bank run contagion will kick off and Circle’s other banks are at risk. I don’t want to discount this to zero and USDC would be an imperfect but plausible way to play that. I don’t like that trade and wouldn’t do it, but I can’t say nobody is using it this way.

So is Circle Okay?

The reality is they have most of the money, unless the US treasury nukes, in which case I don’t think the stablecoin is really our biggest problem. It may take them time to process all the withdrawals, as if market makers and hedge funds were loading up on USDC over the weekend they could see a shelf of over $10B of redemptions to close the gap. It’s entirely possible this will happen and Circle’s business is about to get absolutely wrecked.

But it’s also very unlikely they don’t have at least a large supermajority of the money. This is the nice part of a fully disclosed stablecoin. You know what is there. We should have more clarity this week, so stay tuned on this space.

Austin Campbell is the founder and managing partner of Zero Knowledge Consulting, as well as an adjunct professor at Columbia Business School. He has previously run the stablecoin platform at Paxos, run trading desks at JP Morgan and Citi, and been a portfolio manager at Stone Ridge, the parent of NYDIG. Austin has been in crypto since 2018 and has been trading and structuring profoundly weird financial instruments for decades.

This usually doesn’t turn out to be more, but assuming higher yields mean higher total returns because you ignored the risk is apparently standard practice in fixed income now? This is the kind of thing I used to lose my mind over when I ran a trading desk at JPM.

At more than one past job, I have had to explain that just because a fixed yield t-note 4 years forward is higher than the 3mo t-bill, it does not mean you will earn more holding that than owning t-bills for that whole duration. No I will not name names.

This is not precisely correct and is a rule of thumb, ignoring things like convexity as well, but what it means is if you have a 3-year duration bond and rates change by 1%, that bond will change in price by 3%.

This is the legal definition of person, so a corporation is one “person”, but a married couple is two. Don’t ask me about married corporations.

Sadly this doesn’t mean they were old people (though they might be!); it means that in a bankruptcy they collect recovery value before the equity holders do.

And if you haven’t and you got this far in this piece, I’m genuinely impressed.

Legal persons, not 2-legged persons

Specifically those over FDIC limits

Yes that’s a real thing and no I will not be able to explain in without a 10,000 word post