Structure Matters

Getting the Details Right for Crypto

This morning, I am seeing an awful lot of angst about the latest proposal from New York State about crypto regulation, up to and including tweets about how this will be the end of crypto in New York.

I think all of this is profoundly misguided.

I want to start with a quick breakdown of what this proposed framework is actually calling for:

Eliminating Conflicts of Interest

Specifically, the bill says the following about interconnected activities:

Preventing common ownership of crypto issuers, marketplaces, brokers, and investment advisers and preventing any participant from engaging in more than one of those activities;

Preventing crypto brokers and marketplaces from trading for their own accounts;

Prohibiting marketplaces and investment advisers from keeping custody of customer funds;

Prohibiting brokers from borrowing or lending customer assets; and

Prohibiting referrals from marketplaces to investment services for compensation.

I am going to be blunt for the crypto crowd: this is all extremely normal in traditional finance.

It should be standard practice that exchanges and brokers do not trade against their customers with knowledge of order flow. It should be standard practice that centralized marketplaces aren’t also the custodian (this is how FTX happens!). It should be the case that brokers can’t lend out customers assets (or at least not without express permission and a better regulatory structure than just being a broker). Undisclosed referral payments or those with inherent conflicts of interest should be prohibited.

This is all very normal and reasonable. There’s no good reason that the exchange should get to issue tokens that they trade on the exchange with insider knowledge; there’s no good reason for exchanges to trade against their own customers; there’s no good reason not to use an external custodian with verifiable balances so you know your exchange isn’t selling all the BTC and yolo’ing into shitcoins.

The last one is a step beyond so-called “proof of reserves1”, in that it actually creates a binding legal structure where the customer assets belong to the customers, at a totally different firm with a fiduciary duty and legal requirement to return those assets.

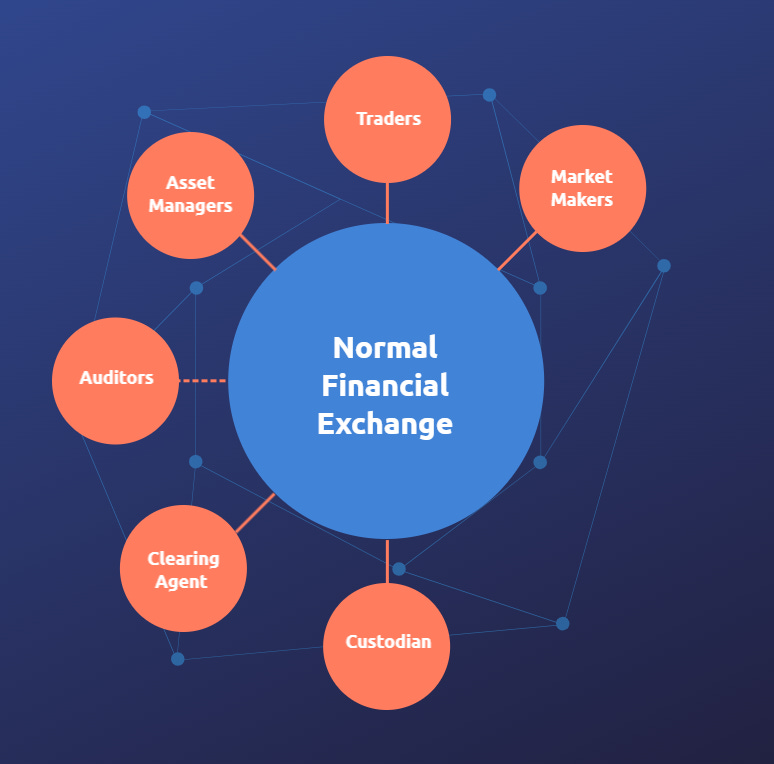

One of the big problems with crypto is how we currently structure exchanges. First, in traditional finance, this is basically how things work:

What this means is that there is separation of duties and legal responsibilities, and it’s quite hard for the exchange to abscond with people’s money (because you’d need to compromise the custodian and the clearing agent as well!). Also, notice the exchange is not trading against its own customers (another big no-no).

So how does it work in crypto?

And we wonder why regulators have a problem with the space?

Seriously, look at those two diagrams and think, for a moment, about what we have done. Crypto, a space ostensibly founded on decentralization, self-custody, and breaking away from the legacy system, is somehow responsible for the creation of the most centralized, trust-dependent financial entities on the entire planet (outside of possibly central banks), and is now defending them from a regulatory proposal that would make them more decentralized?

Mandatory Auditing and Financial Statement Disclosure

Again, this is pretty normal stuff. Here, there is going to be something of a bar that favors incumbents with some degree of scale. On that front, I could make the argument that these requirements should either be lighter or perhaps dependent on time in operation / scale of assets so that you don’t capture startups on day one into a system that requires huge spend with a big 4 auditor.

On the other hand, once you have some degree of scale, shouldn’t there be some independent oversight? “Hey we are totally not ripping you off, trust us” is not a system that anyone should rely upon. It was a problem for FTX. It was a problem for most of the lenders. It will be a problem again in the future.

If you want to handle other people’s money, but you also don’t want anyone able to monitor your behavior with other people’s money, some questions should probably be asked.

The complete aversion of some exchanges to this is likely indicative of problems, I would add. Given my background in financial risk, where there is smoke, there is often fire. If an exchange stridently won’t comply or their compliance is facial at best while hiding the key details, you should be exceptionally skeptical of them.

Financial Controls and Investor Protections

There is another large segment of this bill around these issues, and it basically works as follows:

Enacting and codifying “know-your-customer” provisions, meaning brokers would have to know essential facts about their customers, and requiring crypto brokers and marketplaces to only conduct business with firms that comply with KYC provisions;

Banning the use of the term “stablecoin” to describe or market digital assets unless they are backed 1:1 with U.S. currency or high-quality liquid assets as defined in federal regulations; and

Requiring platforms to reimburse customers who are the victims of unauthorized asset transfers and transfers resulting from fraud.

Again, pretty normal financial stuff. Most places should have KYC/AML for dealing with clients in a centralized fashion. Having your stablecoins actually be stable would be great. In traditional markets, most platforms do retain liability for fraud and other financial misdeeds, so that they can’t just punt on controls and then pass the damage on to their clients when bad things happen.

This is also very normal.

Problems With the Bill

So with that said, I see a number of problems here, but they are mostly not the problems I see being raised (with one exception, in the case of fellow professor Drew Hinkes, who sees some of the same problems I do) in public right now, where people are acting like causing an exchange to break apart is some kind of heresy and extreme centralization is a natural right.

So what are those?

First, we need to be careful about who these provisions apply to. NY state will need to be exceptionally clear when crafting this, as this legislation should 100% apply to Coinbase, Gemini, Binance.US, etc., but it should 100% not apply to Metamask, Uniswap, or so on. People who are providing a centralized service in the regular way and handling the customer funds are precisely those who should be bound by the kinds of controls we need for trusted, centralized intermediaries.

Those are not the kinds of things we need to apply to actually decentralized software deployments, especially those which are immutable2. Drafting this will be key to avoid breaking a bunch of things that are not actually in scope from a first principles perspective.

Second, we need to make sure these services can actually be provided. In the case of audit and accounting, what are the standards they are being held to and how are those services to be provided? If you tell all the exchanges you must be audited, and then all the audit firms turn around and say no thanks because there are not AICPA standards or some such and refuse to audit due to lack of clarity, do you know what this bill actually is? A ban! To that end, all of the requirements should have feasibility attached to them, such that if an exchange attempts to retain auditors in good faith and the audit community will not do so, then the exchange is allowed to be out of compliance because the services literally cannot be provided. When that market matures, they should have to do it. Similarly, it would probably be a good idea for NY to spell out some standards they expect here so people have something to point to and build around.

Third, we need to make sure this is not accidentally a financial death penalty. A good example there is in the case of covering acts of fraud. Most firms have insurance for this, but guess what? The crypto insurance market basically doesn’t exist. Now, maybe this will help create it because people will be forced buyers, but again, one should make sure this works properly. With no insurance, you don’t want exchanges going to bankruptcy every time there is a hiccup in this space, because that helps nobody. Properly regulating custodians would help, but also important here is the knowledge that the OCC is currently blocking custodians in this space (see none of the custodial banks nor private entrants having any success), so mandating a thing has to be used and then banning the creation of the thing is again a ban. NY basically needs to have their own custodial legislation with a mandate for the NYDFS to get moving and approve some of those post-haste if they want to pass this and require custodians. Again, a phase-in approach is probably the key to this kind of requirement as well. Doing it with immediate effect would, actually, kill crypto in NYC.

Conclusions

Overall, I think this is a good starting effort by NY state on some financial market standards, with the caveats that they need to apply it to the right players, they need to make sure the services required can actually be offered, and that they give adequate time for implementation.

I think the most important part is the ban on certain types of commingled services (we have known for a long time these are problems in traditional finance). Let’s not beat around the bush - this is a dramatic restructuring of the industry and will take a lot of work. However, I think it’s a necessary restructuring, as this sort of change is how you prevent another FTX situation. Financial conglomerates that control all of the levers of a system are invariably used to abuse people over time, either in overt ways (FTX) or less obvious ones (extremely high transfer pricing, etc.). If we care about decentralization and reducing monopoly power, we should be supporting this kind of implementation as an industry.

Therefore, I view this as a surprisingly constructive starting point. I think the key will be engaging with NY to discuss actual feasibility, as a jump-to-compliance before services exist and transition plans can be created would be catastrophically dumb, but equally bad would be just acting like the problem will magically go away on its own and that insanely centralized exchanges are an acceptable financial structure in this space.

Austin Campbell is the founder and managing partner of Zero Knowledge Consulting, as well as an adjunct professor at Columbia Business School. He has previously run the stablecoin platform at Paxos, run trading desks at JP Morgan and Citi, and been a portfolio manager at Stone Ridge, the parent of NYDIG. Austin has been in crypto since 2018 and has been trading and structuring profoundly weird financial instruments for decades.

Which are not actually proof of anything unless you have absolute certainty the assets present are not encumbered nor legally allowed to be encumbered in any way and cannot be swept into a bankruptcy, but rather only returned to customers

I think there’s a better argument than most realize to apply these to upgradeable smart contracts