Binance vs. SEC

Binance vs. SEC

A Continuation of Previous Themes and Bad Behavior

Today, the SEC disclosed their latest broadside against the crypto space, and there have been a number of takes flying around with regard to it. Despite the fact that my writing is dire enough to convince some, I am not a lawyer myself, so I wanted to read the entire thing and then respond with thoughts on how this impacts the business of exchanges, crypto, and what the long-term effects will be for the space.

Let there also be this important caveat: everything here is based only on allegations from the SEC. We have not seen a response from Binance and they have not yet had a chance to defend themselves. Neither party in a lawsuit deserves unconditional belief or the ability to make facts up that are not true, so please take everything here as a hypothetical possibility until more facts emerge. They are, for now, just allegations.

Also, perhaps, why I think the effects will be long-term given the current political situation in the United States.

Summary of Claims

There’s a lot going on inside this document, so I’m going to try to summarize in a way that is understandable to a normal two-legged human being.

First, in terms of allegations, the SEC is stating the following:

Binance operated in the United States as an exchange, clearing agency, and broker dealer with regard to their exchange operations.

Binance has directly acted as the issuer / in a material partnership regarding securities with thinly disguised language around BNB and BUSD1.

Binance has facilitated trading of other crypto assets on their platform

Binance has lied, misrepresented, and obfuscated the actual activities of their legal entities such that they were:

Faking volumes on some exchanges

Engaging in trading against their own customers

Lying about / fabricating controls

Faking the independence of Binance.US

Note that the SEC having authority over these things is predicated upon them being securities. The S in SEC stands for the Securities and Exchange Commission, after all. With that said, even if the assets are determined not to be securities and that the SEC does not have authority (a thing that is going to take years to determine, and also one where the collateral damage in the meantime is going to be significant - more on this later), the conduct in bullet number four is clearly impermissible if true and the structural issues in bullet one are something that I have talked about before in the crypto markets.

Put differently, even if I have harsh words for the SEC at times and think they are being profoundly damaging in their approach, that does not mean that everything they say is incorrect or that there is no merit to various accusations. It can be the case that both things are true at once.

To that end, let us go through these in order.

Binance operated in the United States as an exchange, clearing agency, and broker dealer with regard to their exchange operations.

What does this actually mean? In a normal financial arrangement, when you have an exchange, that exchange does not do everything. They are not typically the custodian, they do not typically clear or settle the trades, and they are not the brokers going out and facing customers (as the usual path is customer to broker to exchange; you don’t directly transact with the exchange as a retail trader in the US).

Now, ignoring the broker dealer part (as with crypto, it is possible and feasible to deal directly with the exchange), this does raise an important structural point:

The fact that exchanges are the exchange, the custodian, and the clearing agency all at once is a bit uncool. What this means is that centralized exchanges (CEXs) in the crypto space are among the most centralized financial entities in all of existence. They take many things that are done independently elsewhere, with checks and balances through the fact that they have different responsibilities, and glue them together into a single horrifying Frankenstein. Note that this has absolutely nothing to do with crypto or blockchain. The fact that we operate this way is a structural choice that has nothing to do with the chain itself; this is off-chain activity.

Is this good? I would suggest no. This sort of centralization is part of what allowed FTX to persist for as long as it did. There are better structures where these things can be separated and crypto would do well to adopt them.

However, is this something the SEC should police? Only if these things are securities, and even then, there will need to be rulemaking and guidance because the current acts the SEC authority is based upon, which are very old2, don’t exactly work with how this would be done on a blockchain. Much better would be legislative clarity, which is what the original acts creating the SEC were written for.

Binance has directly acted as the issuer / in a material partnership regarding securities with thinly disguised language around BNB and BUSD

This one is a bit more interesting to me. First, to dispense with the ICO point, it is entirely possible to me that depending on the terms and conditions of the original distribution of BNB, it could have been a securities offering.

However, if so, in their own complaint, the SEC points out that the offering price was $0.15 and it has traded as high as >$300. I’m going to have a hard time finding some theory of damages here that is going to be particularly persuasive to a judge. If anyone damaged investors, it was the SEC nuking BNB prices today with this filing, but even then, if you were in the ICO, you are way, way, way up.

Now, as a matter of conduct, should people not be doing unregistered securities filings? Yes. I do agree with that. But when we get to the section on relief being asked for, let us remember this: they are upset paperwork wasn’t filed when investors clearly got rich.

A secondary point, one which my friend Lewis Cohen has spoken about far more eloquently than I ever could, is if BNB is still a security even if there was an initial securities offering. Here, my answer is “…uh, maybe?”, but we would have to see a lot more facts than what are in this filing for there to be a clear answer on that.

Now let us move onto BNB. The relevant section there is as follows:

First of all, to give readers a tenor of how petty and tenuous elements of this filing by the SEC are, let’s first start with the “purportedly” backed part.

BUSD, to be clear, is issued by Paxos Trust Company3, which is an NYDFS regulated trust company that has pretty strict rules around the management of reserves, replete with risk and controls requirements as well as disclosure requirements. In my time at Paxos, we moved to absolute best-in-class reporting on the assets backing the stablecoin.

In different words, the “purportedly” there is accusing Paxos of fraud and accusing the NYDFS of failing to regulate the reserve. To the best of my knowledge, and with certainty for my time at Paxos, not only was all the money there, it’s actually the only one of the major three stablecoins (along with USDC and USDT) that has had zero doubts about the reserve and been at the forefront of both disclosure and safety.

For the SEC to come out and make a statement essentially falsely accusing another US regulator of malfeasance is pretty beyond the pale. If they meant something else, they should have said it.

Second, the argument for why BUSD is a security is quite expansive. The theory that all it takes is a commercial arrangement where there is profit and an intent to distribute is extremely broad. Agreeing to help with listing and distribution, and profiting from that, is basically how… things work?

I’m going to be interested to see how the rubber meets the road on this one with a judge. I do agree it’s possible there could be some sort of investment contract, but for that to make BUSD the security itself is pretty much the exact opposite of the original finding in Howey (spoiler alert: the oranges are not securities). For something to be the product of an investment contract does not make it investment contracts all the way down4.

This is one area where I will be watching the result very closely, as a finding that this sort of arrangement is specifically a security could implicate all kinds of things that we are not currently thinking about as securities in the United States, and also puts the SEC perilously close to stepping onto the turf of banking regulators if they push the money angle of this argument.

If nothing else, it’s a previously undisclosed view that a specific type of activity engaged in by many parties (for example, almost the exact fact pattern alleged here would also apply to Starbucks profiting off user funds for Starbucks gift cards or their app) that magically sprung up through an enforcement action rather than any rules making.

With that said, like the previous point, are there specific activities that were taken with BUSD that could be a securities offering? Yes. I think that’s possible. See my previous comments on BNB. However, does that make BUSD itself a security? Likely no.

Binance has facilitated trading of other crypto assets on their platform

The SEC specifically calls these crypto asset securities, a term that is not actually a legal term but just a way of saying it’s a security. What confuses me about this is the list of assets they picked to target, other than the aforementioned BNB (maybe) and BUSD (…sigh).

They are:

SOL, ADA, MATIC, FIL, ATOM, SAND, MANA, ALGO, AXS, and COTI

I genuinely have no idea what is going on with this list. It’s like a robot randomly generated a list of tokens and decided to go after them. There are some of the layer 1’s on the list (SOL, ADA, MATIC, ALGO, ATOM), but… FTM is not on there, AVAX is not on there, and more notably, LUNA is not on there. Yet some of those have the exact same characteristics and arguments as the things listed?

Did they just do a few and stop? Were they not aware of the existence of other tokens? Do they inexplicably think that FTM is not a security but ALGO is? Do they think some of them lack a US nexus? Did they just forget to include, oh I don’t know, the one where investors and consumers were actually badly damaged and they would have the best claims!?

This is the work of a madman.

Do you know why this is also so inexplicable?

Because it is 2023, and the SEC has still not publicly written a clear statement or made rules on what makes a token a security or not. They do not tell people what features they use to determine them. They do not explain how they are making determinations that seemingly apply to many tokens but are only naming a few. They don’t tell you how to register (everyone that has tried has failed, either by registering in a way that makes them illegal and thus shutting down, or failing to register).

It is, to say the least, confounding. Certainly, for a regulator charged with investor protection, consumer protection, and capital formation, it’s a path to likely achieve literally none of those goals.

Binance has lied, misrepresented, and obfuscated the actual activities of their legal entities such that they were…

So I want to be clear on this list of things: if there is truth to the allegations being made here, then whether the SEC is the correct regulator or enforcement authority for this action or not, these are bad.

Some of them are very bad.

I would say the minor ones are commingling if it was purely operational mistakes, and the whole issue of independence of people when you report up a chain to ultimately the same executive as other entities.

The medium ones would be the wash trading (not actively harmful, but clearly deceitful market conduct and something that should not be occurring), commingling of funds out of laziness or convenience, and if the independence was fake and a shield to block things out of paranoia they would be unfairly targeted in the United States.

The very bad ones would be the whole lying about controls that did not exist (inexcusable in any context), commingling funds to specifically engage in activities that you had said you were not engaging in, or if the independence was always fake and these were known puppets where even the employees were deceived.

In no context would these things be acceptable, it’s just varying degrees of bad. To that end, I do want to hear the Binance side of the story, and the fact that I have some very pointed criticism for the SEC’s approach does not necessarily mean the other side is a good guy.

If two hardcore criminals shoot each other simultaneously in cold blood, there’s no good guy in that engagement. It’s possible that is the case here. I’m not rushing to judgment because I believe we have the legal process for a reason, and I’m still not convinced the SEC is the right regulator, but I do want to be clear that if the conduct here is as alleged, it’s somewhere between bad and very, very bad. It should not be allowed to continue or ignored.

What Does the SEC Want?

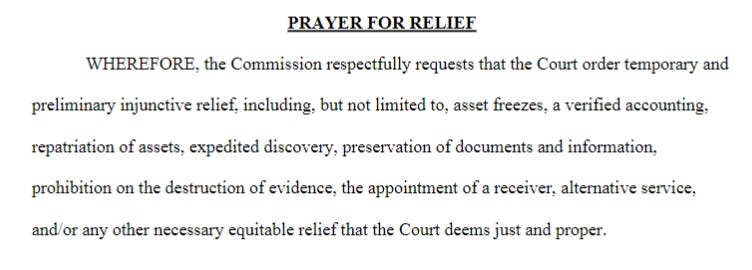

So based on that, let’s look at what the SEC is asking for in terms of preliminary and final relief.

Let’s be very clear about what this means:

They want Binance to be bankrupted and shut down as part of the temporary and preliminary relief. This is the kind of thing you ask for when the conduct is so bad that it’s a clear and present danger to everyone involved for it to continue for even one more second, and the collateral damage doesn’t matter.

Why do I say that? Note the part about asset freezes, repatriation of assets, and the appointment of a receiver.

That is what you do when you kill a financial institution. None of that, I repeat none, is about anything other than putting something to death. This is a bald-faced ask that, as a temporary injunction before any real activities have occurred, a court shut down Binance purely on the speculative say-so of the SEC.

This seems inappropriate. If they have cards that show Binance is actually a ponzi scheme actively damaging customers right now in the sense of FTX5, or that there is a clear and present danger that Binance has misappropriated all the user funds in a way that would justify this action, they need to say that in a filing. They have not.

Without that, killing Binance or crippling it in this way would, with certainty, damage investors, damage customers, and benefit basically nobody. They are basically threatening companies with death for not bowing down to regulation by enforcement.

Gary Gensler: (Michael Palin) (looking round office casually) You've... you've got a nice

army basecrypto exchange here,ColonelBrian.Brian: Yes.

Gary Gensler: We wouldn't want anything to happen to it.

Brian: What?

Dan: No, what my

brotherchair means is it would be a shame if... (he knocks something off themantellisting page)

This is how you know how extreme the position is: the people that the SEC is purporting to protect with this action are the ones who would actually be harmed the most as their assets collapse in value because the SEC itself killed the value.

“Pay up or we destroy you” is the conduct of thugs and criminals, not legitimate regulators.

The other relief they ask for, which are at least not insane, basically involve kicking Binance and CZ out of the US and never letting them operate here, as well as civil penalties for the misconduct and lying. These I agree with - if they are guilty as charged, then these are fitting penalties.

That first part, though.

Implications for the Space, Customers and Investors

What do I take from this as a businessperson, as ultimately, that’s what I care about?

I would say the following:

First, don’t assume the SEC intends to make rules or act openly until they sue. If you operate in the United States, they will take insanely broad maximalist stances (see the BUSD as security argument), and if you don’t play ball with them, they will file things like this about your business. Here, there are also allegations of very real misconduct, but this has not always been true elsewhere (LBRY anyone?).

Second, given the US political stasis, the only fix for this currently is the courts. If 2024 is a landslide for the Republicans (or a very different Democratic president), then maybe we get a change a full year after that. So at the earliest, we are talking roughly 2.5 years of continued litigation and enforcement by regulation. The only path to clarity will be through the courts, and that is also a path where one has to be aware judges do what they think the law says and permits6. It’s entirely possible you get a very left field ruling on crypto that is crippling to both the SEC and the sector if you push your luck.

Third, given the lack of compliant trading venues in the United States if the SEC’s theory is true, we could be in a world of hurt for retail crypto traders. Nothing would be more devastating to the investors that the SEC is purporting to protect than if they actually forced all the US exchanges to shut down and people could not trade their crypto. However, given the path they are proceeding down is one where it does not appear to be functionally possible to trade crypto (there are zero clearing agencies, for instance, who can touch it based on current rules, and they just said people have to “register” as one), the SEC’s current theory of crypto amounts to a complete ban in the United States and people should be aware of that.

To that end, note that the market for non-security crypto assets (even those the SEC has not called securities, like BTC and ETH) are down significantly on this news. If you believe that information is priced in, the market seems to understand better than the SEC itself that the current SEC path damages, not protects, investors.

I continually advise my clients in this space to avoid the United States for now. Things like this are why; when you don’t have to take on this kind of risk, why would you? The loser will be the United States.

With that said, there is very little new in this filing. It’s just a continuation of themes the SEC has been banging on about for three years: everything is a security, you have to come in and register, but also our requirements are that to register, you have to stop doing crypto and just do traditional securities. And if you don’t, we’re going to burn your house down.

Legitimate vs. Illegitimate

So why am I writing this post, and why is my reaction to this filing so negative?

The core problem here is one of legitimacy.

Again, I want to re-iterate the point that I am not necessarily supporting Binance. If some of the actions are as alleged, they should not be permitted and there should be consequences.

What I am against is the following:

Regulators making up the rules as they go and refusing to provide clear notice for people to understand what they are. Legitimate rules are transparent and understandable. If I park where I am not supposed to and it was clearly marked, I deserve the ticket. If there is no signage, no way to know, and it depends on a subjective determination by a parking officer, that’s not legitimate and is a pathway to corruption and collapse of rule of law.

I am against regulators going rogue. Unless you are okay with operation chokepoint 3.0 under the a future extreme administration targeting immigration attorneys, abortion providers, liberal media organizations, public sector unions, and electric vehicle manufacturers because they are high risk activities, you should not support the SEC’s conduct here. Unless you are okay with a future administration doxing every single vendor or counterparty of a financial product to intimidate them without any legal process, you should not support the SEC’s conduct here. Unless you are onboard with extending legal theories to what is convenient so that any company in America can be a target at any time for enforcement based purely on the whim of an unelected bureaucrat, you should not support the SEC’s conduct here.

Lastly, when you ask for relief, clearly state the claims and have that basis be grounded in reality and based on your mandate. If you are charged with investor and customer protection, don’t ask for relief where the primary effect of the relief is to nuke investors and customers from orbit while you cackle maniacally and tell people you are protecting them. This is Bond villain level conduct.

There could have been a more narrow complaint against Binance for basic consumer protection issues that could have been filed. Maybe that would not be the SEC alone, or maybe they would have had to cooperate with another federal agency (like the DoJ) in order to do this effectively. They did not. They went big, with novel theories previously undisclosed or stated (see the token list, again) and enforcement actions designed to intimidate. This is not doing the right thing.

This filing is not about consumer protection.

This filing is not about investor protection.

This filing is about power.

Austin Campbell is the founder and managing partner of Zero Knowledge Consulting, as well as an adjunct professor at Columbia Business School. He has previously run the stablecoin platform at Paxos, run trading desks at JP Morgan and Citi, and been a portfolio manager at Stone Ridge, the parent of NYDIG. Austin has been in crypto since 2018 and has been trading and structuring profoundly weird financial instruments for decades.

If you want an example of petty and inappropriate legal behavior, calling Paxos Trust Company A while providing clearly identifiable details about Paxos so it’s not anonymous at all is exactly the kind of thing you’d look for to see if someone is deliberately flaunting norms and rule of law to score political points

The 1940 act was written closer to the Civil War than the current day!

See footnote 2 for the fact that this is also way out of bounds

Sorry, turtles

Who the SEC was meeting with and using as an example to create rules based on, hilariously

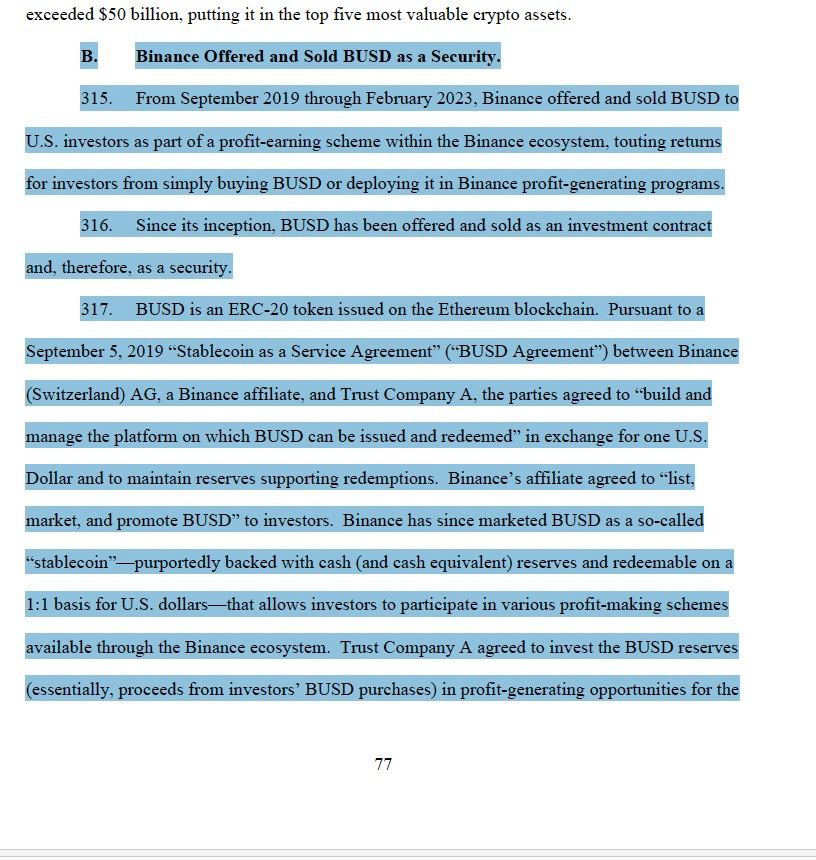

Just wait until a super originalist judge points out nothing in the 1940 act authorizes securities trading on the internet so that all has to go or something equally wild